Lawrence Gulotta is a New York-based observer of Israel who is informed by a background in real estate economics and affordable housing finance. His most recent article for the blog of Dissent magazine is “Starchitects in the Promised Land.” Mr. Gulotta has submitted this article especially for the Partners blog, being posted here in two parts, beginning as follows:

A Matter of Housing Equity by Lawrence Gulotta

Gentrification and housing affordability are contentious issues in Israel’s major cities. The sales prices of apartments, and rental rates, have experienced a striking increase. The Jerusalem Post, no lefty newspaper, proclaims: “Homes prices in Israel are unquestionably among the highest worldwide when looking at price per square meter.”According to the Bank of Israel, the price of the average Israeli home has risen nearly 50 percent since December 2007 with rent prices also climbing sharply. Over the past year alone, apartment prices have risen 15 percent in some urban areas. The real estate bubble has created new and deeper social class stratification among Israelis, in an already polarized class structure.

Only the wealthiest 30% of Israelis can afford to buy a home and take out a reasonable mortgage to do so, according to a Technion-Israeli Institute of Technology study by Drs. Danny Ben-Shahar and Yakov Varshavsky of the architecture and town planning faculty.

This group qualifies at the currently institutionally accepted “loan-to-value ratio” (“LTV”) for a residential mortgage loan of no greater than 60% of the asset’s value. The income to debt service plus maintenance costs ratio is not to be greater than 30% of the buyer’s income. The loan to value ratio is defined by the Appraisal Institute as “The ratio between a mortgage loan and the value of a property pledged as security, usually expressed as a percentage.” The equity ratio is defined as “The ratio between the down payment paid on a property and its total price” also expressed as a percentage.

The study found that half of Israel’s households could buy a home with a mortgage LTV of up to 80% of the home’s value.

A change from one third to one half, or a 34% increase.

The researchers also showed that working class salaries have not kept pace with home price increases over the past 20 years, 1991-2011.

They found that the average home price was equal to 51.7 monthly salaries of a person in the fifth decile; now the figure is 90.7 – a 75% increase, 1991-2011.

The study concludes, “…these findings show the need to consider far-reaching reforms that would drastically alter a households’ ability to buy homes.”

Contrary to the study’s recommendations, the Bank of Israel has tightened mortgage lending terms for loans greater than 60% of the asset’s value. The Bank has raised its reserves, to discourage mortgage lending. It has also reduced interest rates. The US interest rates and the Israeli interest rates for mortgage loans are moving in opposite directions (see schedules below). In the US, a loan-to-value ratio of 60% would be considered a very conservative underwriting guideline. That being said, Israeli homeowners have maintained stronger equity positions in their homes than homeowners in the US and Spain. Underwater mortgages are not a mass phenomena in Israel, like in parts of the United States.

There are secondary markets in Israel for financing a home. First Israel, advertises, “Whether you are making aliyah, looking for an investment, or buying a second home in Israel,” call First Israel. “When purchasing an existing property or constructing a new one, First Israel provides mortgage financing up to 75% of the value of the home. Financing of up to 100% may be obtained for borrowers with equity in additional properties.” First Israel notes, “Obtaining financing for the purchase of a home in some areas of Israel can be difficult.”

The Bank of Israel appears to be lowering its interest rates for mortgage lending. The following schedules are illustrative of the lending rates as of August 2, 2013:

|

Average Rate of Interest on CPI-Indexed Mortgages

|

הריבית הממוצעת על משכנתאות צמודות למדד

|

|

|

|

ממוצע

|

מעל 25

|

מעל 20 ועד 25

|

מעל 15 ועד 20

|

מעל 10 ועד 15

|

מעל 5 ועד 10

|

עד 5 שנים

|

|

|

|

|

|

שנה

|

שנים

|

שנים

|

שנים

|

שנים

|

|

|

|

|

|

Average

|

More than 25 years

|

From 20 to 25

|

From 15 to 20

|

From 10 to 15

|

From 5 to 10

|

Up to and

|

|

|

|

|

|

Years

|

years

|

years

|

years

|

including

|

|

|

|

|

|

|

|

|

5 years

|

|

|

|

|

|

2.10

|

3.16

|

3.17

|

2.75

|

2.24

|

1.75

|

2.07

|

|

|

|

|

Bank of Israel 8-02-2013

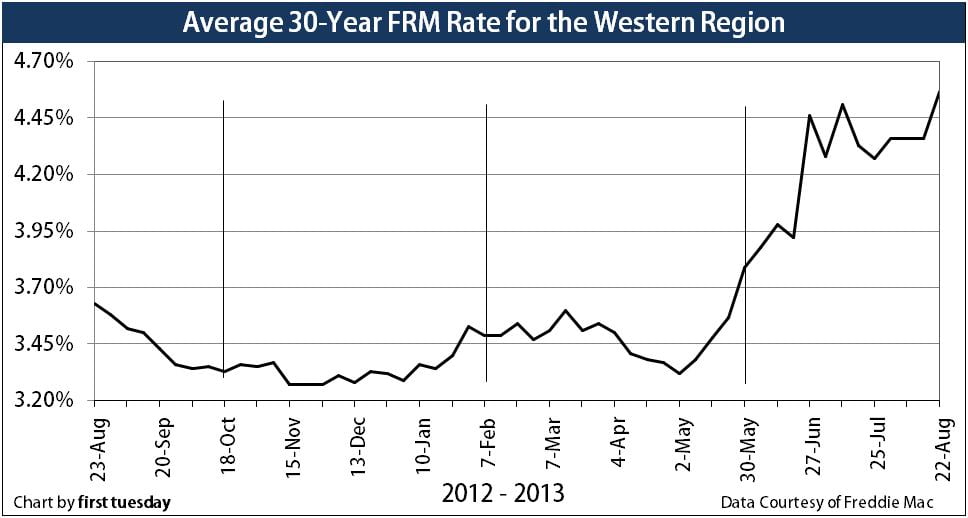

US rates are higher:

|

US-West Average 30-Year Conventional Commitment Rate

|

|

Chart update 08/01/13

|

|

Current

08/01/13

4.36%

|

Month ago

07/03/13

4.28%

|

Year ago

08/02/12

3.5%

|

The average 30-year commitment rate is the rate at which a lender commits to lend mortgage money in the United States-West as reported by Freddie Mac. The western region includes CA, AZ, NV, OR, WA, UT, ID, MT, HI, AK, and GU. More information is available on Freddie Mac’s Primary Mortgage Market Survey report.

|

The ongoing social protest movement in Israel and the center-left political parties have raised their voices over the chronic inability of the average working Israeli family, the young, and senior citizens to afford decent housing. Israelis find it difficult to accumulate 40% of the sales price of a home in cash equity. The 60% loan-to-value ratio imposed by the underwriting guidelines and policies of the Bank of Israel effectively excludes or delays homeownership opportunities for first time homebuyers.

Not everyone is convinced the social protest movement has an answer to Israel’s housing shortage and the challenging first time homebuyer market. In “Dragging Israel Back to its Socialist Past” Jonathan S. Tobin, Commentary, July-August 2013, notes:

If it [Israel] is currently in the best economic shape of its short history, it is because its recent governments have understood there can be no going back to the “social democratic” nightmare that once created multi-year waits for phone installations and other vestiges of a largely state-run economy. As the Jerusalem Post notes in an incisive editorial, the protesters and those egging them on have no coherent program to offer as an alternative to the government’s policies. Instead, all they have are “empty populist slogans articulating nothing more than inchoate discontent.”If Israel is to continue on its current path toward greater prosperity, Netanyahu should stand his ground. While there can be no denying that problems exist and must be addressed, those who care about Israel’s future should not give encouragement to those who are trying to drag the Jewish state back to its troubled socialist past.

Notwithstanding Jonathan Tobin’s admonition that “recent governments have understood there can be no going back to the “social democratic” nightmare that once created multi-year waits for phone installations and other vestiges of a largely state-run economy,” the Israeli government response has been the opposite of Tobin’s desires and understanding of real estate markets and the elusive affordability index.

Nimrod Bousso writes in Ha’aretz, in an article entitled, “Government weighs new plan to set target prices for homes”:

The initiative… represents a sea change in the government’s attitude to the housing market. In the past, it has preferred free market solutions to housing and other industries over more government intervention.

“There’s no doubt that we’re talking about deep regulation on the part of the government, but we face a deep crisis,” said Chairman Bentzi Lieberman of the Israel Lands Authority. He continued, “We have to develop an effective process for lower prices in a situation where the Bank of Israel, by continuing to lower interest rates, isn’t helping.”

Jonathan Tobin places his free market ideology above pragmatism and the “facts on the ground.” The problem in Israeli housing is that there is a “troubled present” and not so much a nightmare-ish socialist past. The Netanyahu government is finally beginning to understand the dimensions of Israel’s current housing crisis and the need for proactive intervention. Click here for Part 2 …

Leave A Comment